Background

In the first part of the series, we covered the FIFO accounting method. CTRM systems have a difficult time tracking the FIFO layers in combination with several common place scenarios such as ‘in transit’ inventory, Gain/Loss adjustments, and prior period adjustments. The WACOG method is easier as there is no layering involved, but the same system pitfalls for the FIFO method impact the WACOG method as well.

WACOG

The ‘weighted average cost of goods’ or WACOG method averages all the purchases and beginning inventory and assigns the average unit cost to the sales for a given period. The method is not as sensitive to rising or falling prices as newer costs are averaged together with older costs. One main advantage the WACOG method has over LIFO and FIFO in an CTRM system is the lack of layering required. This is an easier method to implement as the system does not have the extra task of tracking thousands of inventory layers which results in more points of failure and additional complex solutions.

Real World Scenario

The scenario below shows two areas where CTRM systems have trouble with inventory valuation. The in-transit movement and the loss adjustment valued at the WACOG price are often not out of the box solutions.

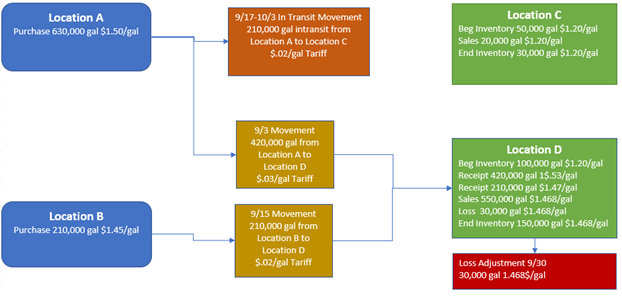

September 2020

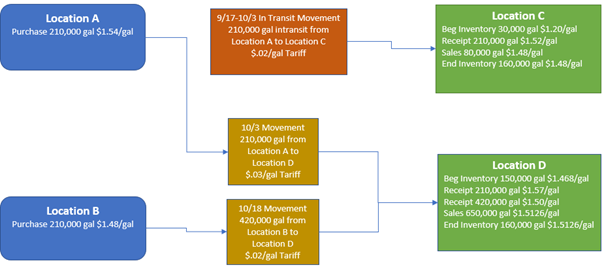

October 2020

CTRM Issues

Some CTRM systems handle the basics of the WACOG method well, but any accounting process that differs from the system is not easily addressable. One example above is the treatment of gains and losses. Often CTRM systems out of the box do not assign value to gains or losses and instead allow the unit cost of the inventory change with a gain or loss. Often accounting groups want to expense gains and losses and will need to assign the current weighted average price to the gain or loss.

Another issue highlighted is the treatment of in-transit shipments. CTRM systems have a difficult time tracking these shipments in their settlement and Mark-to-Market valuations as they cross over accounting and production months. Systems often do not allow for the proper creation of journal entries for the in-transit inventory.

All these issues are compounded when prior period adjustments are added. Tracking changes on already incomplete data becomes a risk that accounting groups are frequently unwilling to take. This prevents firms from utilizing their inventory modules and tracking inventory outside their system. This is not the correct approach. Tracking inventory outside the system in spreadsheets creates additional risk in data quality, human error, and reduced audit capabilities. Lucido Group has the experience and the tools to help. The solutions we have designed in the past have helped customers tackle complex accounting issues like in-transit inventory, gain and loss values, negative inventory, prior period adjustments, and proper automated journal entry creation.

We Can Help

Our team has decades of experience working with CTRM systems and complicated inventory valuation processes. If you are in need of expertise to properly configure or troubleshoot your inventory valuation, please contact us.